The paper is concerned with beliefs about future performances of securities and the construction of a portfolio which can maxmimise returns.

Markowitz is not convinced that an investor can maximize returns without taking variance into consideration or without diversifying their portfolio. Hence he introduces the expected returns-variance (\( E \)-\( V \)) rule. The \( E \)-\( V \) rule states that the investor would (or should) want to select one of the portfolios with the minimum \( V \) for a given \( E \) or a maximum \( E \) for a given \( V \). No where in the paper is it proven that diversification is necessary; it is taken as a given based on observations. Using known statistics and probability theory rules and the assumption that there won't be any short sales, he states the expected return \( E \) and variance \( V \) of a portfolio consisting of \( N \) securities as \[ E = \sum_{i=1}^{N} X_i \mu_i \tag{1} \] \[ V = \sum_{i=1}^{N} \sum_{j=1}^{N} \sigma_{ij} X_i X_j \tag{2} \] \[ \sum X_i = 1 \tag{3} \] \[ X_i \ge 0 \tag{4} \] where, \( X_i \) is the percentage of the investor's assets allocated to the \( i^{\text{th}} \) security, \( \mu_i \) is the expected value of the \( i^{\text{th}} \) security, \( \sigma_{ij} \) is the covariance between the returns of the \( i^{\text{th}} \) and \( j^{\text{th}} \) security, \( X_j \) is the percentage of the investor's assets allocated to the \( j^{\text{th}} \) security,

Definitions

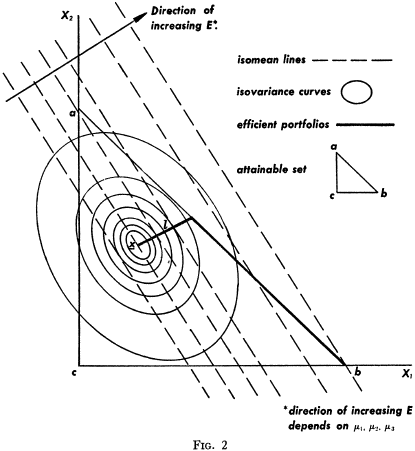

- Attainable set: of portfolios consists of all portfolios which satisfy (3) and (4).

- Isomean curve: is the set of all points (portfolios) with a given expected return; are usually a system of parallel lines.

- Isovariance line: is the set of all points (portfolios) with a given variance of return; are usually a family of concentric ellipses.

- X: is the center of the above system of isovariance ellipses which denotes minimal variance \( V \).

- Critical line: is the locus of points that minimise variance for each given expected return \( E \).

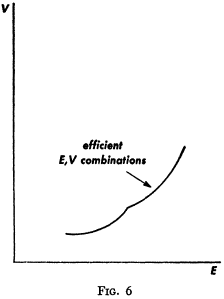

The \( E \)-\( V \) principle can be used in theoretical analysis or in the actual selection of portfolios. If used in the selection of securities, statistical computation can be used to arrive a tentative set of \( \mu_i \) and \( \sigma_{ij} \). One way of arriving at a tentative set is to use the observed \( \mu_i \), \( \sigma_{ij} \) for some period in the past. Judgement could then be used in increasing or decreasing some of these \( \mu_i \) and \( \sigma_{ij} \) on the basis of factors or nuances not taken into account by the formal computations. Using this revised set of \( \mu_i \) and \( \sigma_{ij} \), the set of efficient \( E \), \( V \) combinations can be computed, the investor can select the combination they prefer, and the portfolio which gives rise to this \( E \), \( V \) combination can be found.